Finance

January 1, Big City Budgets in Deep Trouble

Wyatt’s Take

- America’s five biggest cities can’t pay their bills.

- Taxpayer debt in places like New York and Chicago keeps climbing.

- Officials are passing costs to future generations instead of fixing the mess now.

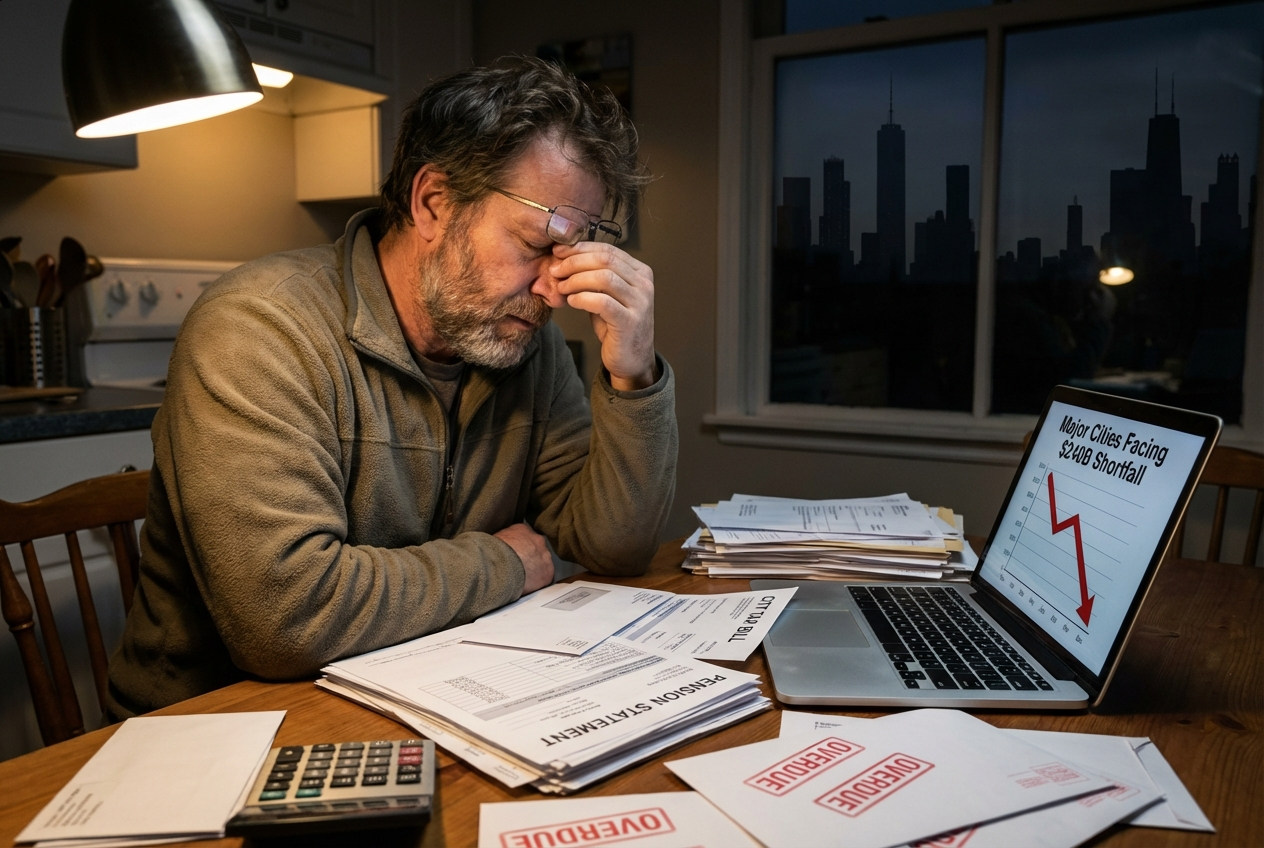

The top five U.S. cities—New York, Chicago, Los Angeles, Houston, and Philadelphia—don’t have enough money to cover their bills, according to a new 2026 report.

The numbers show regular folks are stuck with a heavy burden. In New York City, every taxpayer would need to cough up $61,700 just to zero out the debt. Chicago comes in next at $42,600, followed by Philadelphia at $17,000, Houston at $4,800, and Los Angeles at $1,300 per taxpayer.

The report says the real picture is even murkier because each city counts its debts and assets differently, making it tough for everyday voters to know the truth come election time.

“Because of varying state laws, cities operate under complex and varied governmental structures, making comparisons difficult and reducing transparency,” the report said.

Altogether, these five cities owe $384 billion but only have $144 billion in assets. The shortfall sits at $240 billion, including pension debt and retiree promises, according to the report.

Officials claim their budgets are balanced, but the report says that’s only because they’re skipping real long-term costs and leaving the mess for tomorrow’s workers and taxpayers.

Pension problems are front and center, with costs growing in every city, and no real answers in sight. Short-term market gains might look good on paper, but the debt keeps stacking up, especially for things like retiree health care.

Chicago stands out as a warning, showing what happens when pension debt gets ignored. Assets can’t cover the promises made, and deficits keep piling up year after year.

The report also warns that Los Angeles and Philadelphia, though making some progress, are boxed in by rising costs and big investments, giving them little wiggle room if things get worse.

On top of all that, New York and Chicago both earned failing grades for their financial health. Philadelphia got a D, while Houston and Los Angeles got Cs.

The experts behind the report say it’s time for local leaders to give honest reports and for Congress to step in and protect private pensions. Regular folks and the media need to keep the pressure on city leaders to clean up their act.

Read more about how these debts affect your community and what’s at stake for your family.

Wyatt Matters

Big city spending and poor management always trickle down to working-class people. This is why transparency matters—so families in the heartland aren’t forced to pay the price for urban missteps down the line.

-

Entertainment3 years ago

Entertainment3 years agoWhoopi Goldberg’s “Wildly Inappropriate” Commentary Forces “The View” into Unscheduled Commercial Break

-

Entertainment2 years ago

Entertainment2 years ago‘He’s A Pr*ck And F*cking Hates Republicans’: Megyn Kelly Goes Off on Don Lemon

-

Featured3 years ago

Featured3 years agoUS Advises Citizens to Leave This Country ASAP

-

Featured3 years ago

Featured3 years agoBenghazi Hero: Hillary Clinton is “One of the Most Disgusting Humans on Earth”

-

Entertainment2 years ago

Entertainment2 years agoComedy Mourns Legend Richard Lewis: A Heartfelt Farewell

-

Latest News2 years ago

Latest News2 years agoNude Woman Wields Spiked Club in Daylight Venice Beach Brawl

-

Featured3 years ago

Featured3 years agoFox News Calls Security on Donald Trump Jr. at GOP Debate [Video]

-

Latest News2 years ago

Latest News2 years agoSupreme Court Gift: Trump’s Trial Delayed, Election Interference Allegations Linger

Sue

February 9, 2026 at 5:05 pm

Democrats keep spending money you don’t have it’s your free ATM card for what ever you want. Democrats destroyed this country and life support system aren’t going to save it.

Rastus

February 9, 2026 at 6:32 pm

A GOP candidate has to win President in 2028 or money will come in the back door as under Biden if that doesn’t happen.

Paul4756

February 9, 2026 at 5:50 pm

This is not a problem. Just do what the Democrat/Communist Party always does: Just raise sales and property taxes 100%. Problem soled!!!

AG

February 9, 2026 at 9:16 pm

Stop public pensions entirely. Public SERVICE should be public SERVICE in terms of a somewhat low initial base pay and a tightly capped pay ceiling. NO overtime.

People in the government are over paid and there are WAY too many employees.

Line ’em up and count off: A, B, C, D, E F, G…pull one of the 7 letters from a hat and the chosen letter employees are dismissed. Do this every other year for a decade. Slim down government.

There are a couple of exceptions…and those are jobs with “death” attached. Firemen, Police, ICE, etc. I believe our protectors should be honored with higher pay. But they should still have a similar matching investment plan with a potentially higher match than desk workers.

New employees and employees with fewer than 5 years should get a match for their 401(k) or their 403(b) with the opportunity to max out a Roth first. 3% should be paid in by the governmental employer, and then another 3% match for employee contributions.

Employees with between 5 and 10 years of service should have their pension contributions rolled over and then they, too, would just have a matching investment fund like everyone else.

Period. End of story.

That is what public companies do. The government should not be paying wages above private similar wages, nor should they be offering bonuses or reward laziness and so forth.